How to use savings buckets to achieve your lifestyle goals

How to pay off debt and save at the same time

8-min. read

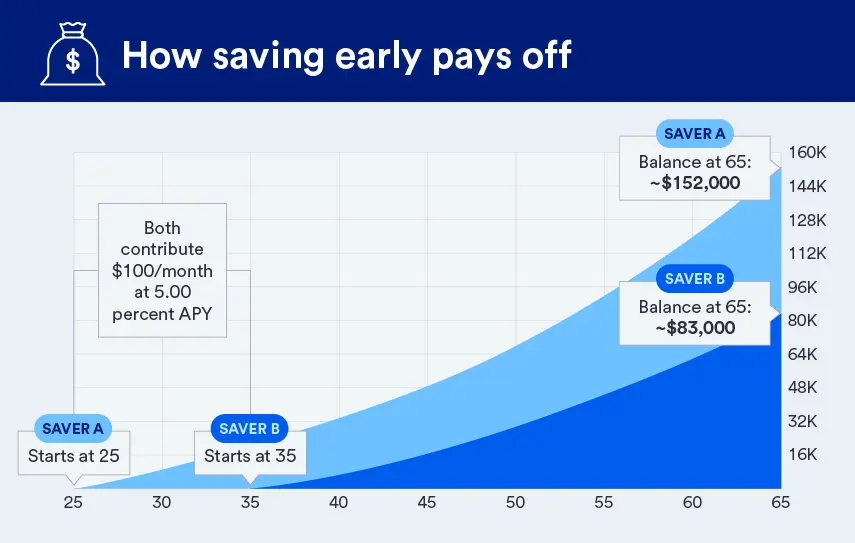

Saving early gives your money more time to grow through the power of compound interest.

The 50/30/20 budget rule can help you balance needs, wants and savings in a way that fits your lifestyle.

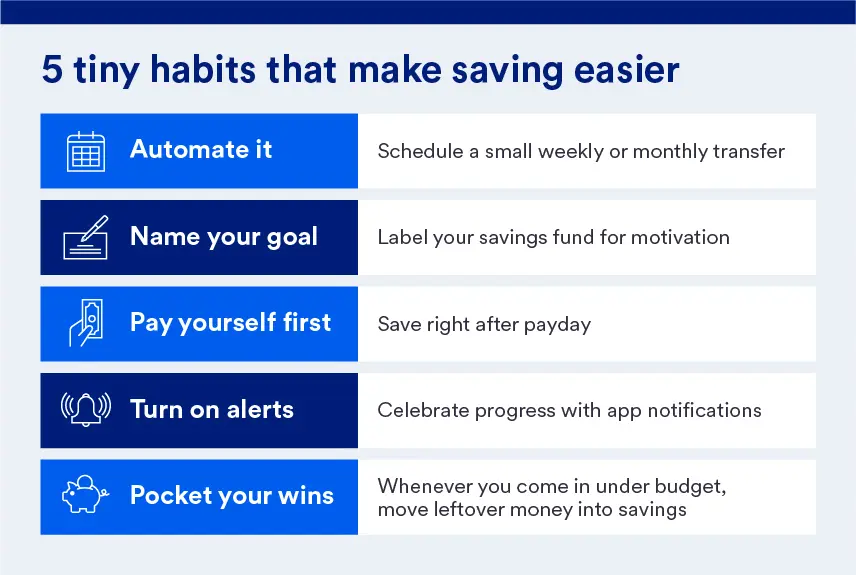

Setting up automatic transfers takes the effort out of saving — consistency matters more than size.

Separate your money into everyday, emergency and long-term savings to stay organized and focused on your goals.

Celebrate milestones and use small motivators to keep your savings habit strong for the long haul.

Saving doesn’t have to mean saying goodbye to fun. Here’s how to kick-start your savings game now — without giving up your favorite splurges — so you can crush your future goals.

There are plenty of financial experts who love telling young adults that they’re wasting money on dining out, coffee, concerts and more, as if guilt is the best way to encourage people to save. But having fun and saving money isn’t an either/or choice. No matter your income, you can live your life and build your future with just a few simple habits, smart systems and mindset shifts.

Any small habit, repeated consistently, will grow over time. The same is true about saving money. For example, let’s say you put aside $25 per week into a savings account. While saving $25 on its own doesn’t sound like very much, at the end of the year, you’ll have $1,300.

And let’s not forget about compound interest — the interest earned on interest. Suppose you have a savings account that earns 3.00 percent APY, compounded daily. That $25 per week becomes $1,328 after one year. Now imagine how much it would grow after 10 years. Spoiler alert: about $14,000.

As you can see, the earlier you begin, the more your money works for you over time.

Just because you know that saving money is a good idea, it doesn’t mean you know how to begin. The good news is that several low-effort steps can help you get started.

A good first move is creating a budget — and the 50/30/20 guideline is flexible and easy to follow (freeing up more of your mental bandwidth). In a nutshell, the goal is to spend 50 percent of your take-home pay on needs (such as rent, groceries, utilities, transportation), 30 percent on wants (such as entertainment or dining out) and 20 percent on savings and debt payoff.

What’s helpful about this guideline is that it doesn’t require exact numbers. You simply need to make sure you’re not exceeding your spending percentage in any category. Additionally, you can always tweak the 50/30/20 to fit your lifestyle — perhaps making it 60/20/20 or 70/20/10 if that makes more sense for you. Not a fan of percentage-based budgeting? Here are several other methods you can try.

Keeping your savings separate from your checking account is also a great way to ensure you’re keeping your nest egg intact. To further avoid dipping into your savings, open a separate account just for that “future you” money. U.S. Bank offers a number of different savings account options to fit your specific needs.

Once you’ve opened a savings account, you still need to actually move money into it. And that’s where automatic transfers come in handy. As the popular saying goes: “Set it and forget it.”

While there’s no single “right” number (what matters is consistency), aim to save about 10 percent to 20 percent of your take-home pay if you can. You can also adjust as you go. If all you can afford to save right now is $50 per month, that’s a great start. Just plan on revisiting your budget in two or three months to see if you can increase your savings rate to $75 or $100 per month. Then do that again in another few months, then again and again until you’ve reached your income percentage goal.

As for how much money you should keep, think of your savings in terms of three buckets:

The exact amounts you put toward each of these buckets will depend on your income, expenses, financial goals and timeline. But financial experts generally recommend keeping three to six months’ worth of essential expenses in your emergency fund, while continuing to contribute smaller amounts toward everyday and long-term goals as your budget allows.

Grow your assets with the U.S. Bank Smartly® Savings account.

One way to bolster your savings is finding lower-cost versions of your more expensive habits or services. For example:

Even while you’re saving money, you can (and should) budget for enjoyment. Fun should always be part of your financial plan.

Turning saving into a game can keep your energy high when motivation dips. One way to do this is by using the savings goal tracker in the U.S. Bank Mobile App to create multiple savings goals. Set up automatic transfers to those buckets and watch as the progress bars grow. Challenge yourself to keep those trackers moving forward every week.

You can also stay inspired by pairing your goals with other visual cues. Saving for a vacation? Set a photo of your dream destination as your phone background. Saving for a wedding? Create a checklist of expenses, and cross them off each time an amount is put aside in your savings.

And finally, celebrate small wins. You reached 25 percent of your goal? Go you! Invite some friends over for a game night, or cook a special meal at home. There’s no need to wait until you’ve finished the race to appreciate how far you’ve come.

If you have high-interest debt, prioritize paying that down first while still setting aside a small emergency cushion. Once your debt decreases, shift more focus toward savings.

A regular savings account works well for short-term goals and emergency funds. For long-term goals, you might consider higher-yield options like a certificate of deposit (CD).

Check in every few months to make sure your goals still fit your priorities. Life changes — your savings strategy should evolve with it.

Base your savings on your average monthly income, and use percentages rather than fixed amounts. That way, you’re saving consistently without overcommitting in leaner months.