Capitalize on today's evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

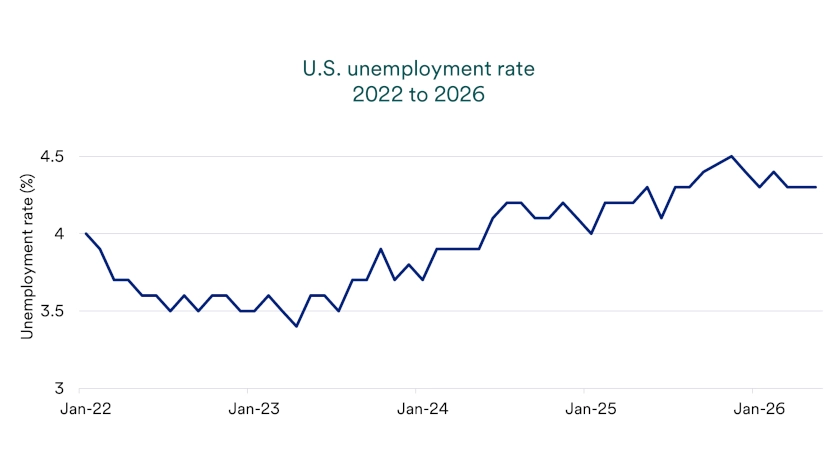

The May jobs report showed a steady U.S. job market, with employers adding 172,000 jobs and unemployment holding at 4.3%.

Wage growth continues to support consumers, but higher inflation complicates the Federal Reserve’s interest rate outlook.

Job openings rose, layoffs increased, and quits stayed low, pointing to a labor market that is expanding recently.

The May jobs report showed a resilient U.S. job market with stronger hiring than investors expected. U.S. employers added 172,000 jobs in May, and the unemployment rate held at 4.3%, according to the Bureau of Labor Statistics (BLS). Hiring gains came from leisure and hospitality, local government and healthcare, while financial activities employment declined.

The report also indicated an improved hiring trend. BLS revised March and April payrolls higher, adding a combined 93,000 jobs to prior estimates, for an average monthly gain of 114,000 per month in 2026, up from just 10,000 per month in 2025. Those revisions make the spring labor market look stronger than the initial reports suggested, even though hiring remains more concentrated than it was earlier in this expansion.

The unemployment rate has stayed within a narrow 4.3% to 4.5% range since July 2025, and labor force participation held at 61.8% in May. Long-term unemployment remained elevated, which suggests people who lose jobs may need more time to find new work.

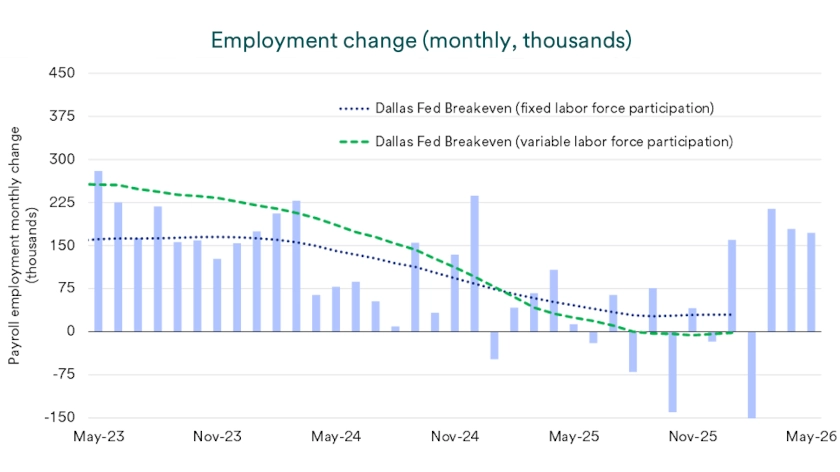

The Dallas Federal Reserve Bank offers a useful lens for interpreting recent payroll numbers. Its March 31 analysis focuses on “break-even” employment growth, or the monthly job gain needed to keep the unemployment rate steady. The Dallas Fed estimates that this threshold has moved much lower because immigration flows and participation trends have slowed labor force growth.

In practical terms, the economy may not need the same monthly job gains it once needed to keep unemployment stable. The Dallas Fed estimated that break-even job growth peaked near 250,000 per month in 2023, fell to roughly 10,000 by July 2025 and moved near zero later in 2025. Against that backdrop, May’s 172,000 payroll gain looks constructive and helps explain why unemployment held steady. 1

Wage growth continues to support household income, but inflation still absorbs part of those gains. May average hourly earnings rose 3.4% from a year earlier, according to the recent employment report. The latest available Consumer Price Index (CPI) report, covering April, showed consumer prices up 3.8% from a year earlier, leaving wage gains close to but not clearly ahead of headline inflation.

“The May jobs report shows a labor market that is still growing, but in a more selective way. Investors should pay close attention to the mix of hiring, wages and labor supply because those details often tell the real story for the economy and markets."

Rob Haworth, senior investment strategy director with U.S. Bank Asset Management Group

Core inflation gives investors a somewhat cleaner read on underlying price trends. The April CPI report showed prices excluding food and energy up 2.8% from a year earlier, below the pace of wage growth. The Bureau of Labor Statistics plans to release the May CPI report on June 10, 2026, so investors will assess the next inflation reading to judge whether pay gains are improving real purchasing power or adding pressure to the Fed’s policy debate.

“The May jobs report shows a labor market that is still growing, but in a more selective way,” says Rob Haworth, senior investment strategy director with U.S. Bank Asset Management Group. “Investors should pay close attention to the mix of hiring, wages and labor supply because those details often tell the real story for the economy and markets.” For consumers, steady employment and rising wages support spending power, while persistent inflation limits how much households benefit from higher pay.

The April Job Openings and Labor Turnover Survey added a mixed but still constructive labor market signal. Job openings rose to 7.6 million in April, while hires fell and total separations declined according to the BLS. The quits rate slipped to 1.9%, showing workers have become more cautious about changing jobs.

This pattern suggests a selective labor market. Employers continue to post openings, but they appear more discerning about turning those openings into hires. Workers also appear less willing to test the market, which can reduce wage pressure over time and keep labor market churn low.

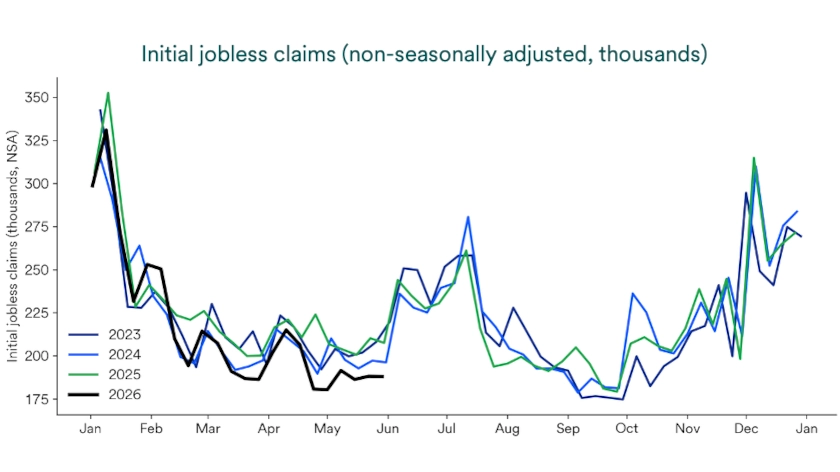

Weekly jobless claims still point to low layoffs across the broader economy. Initial unemployment claims rose to 225,000 for the week ended May 30, while continuing claims were 1.78 million for the week ended May 23, according to the Department of Labor. Those levels remain consistent with an economy where employers are not cutting workers aggressively across the board.

Challenger, Gray & Christmas reported a rise in announced job cuts, but in line with historical norms. U.S.-based employers announced 97,006 job cuts in May, up 16% from April and the highest May total since 2020. At the same time, year-to-date job cuts remained 43% below the first five months of 2025, when federal workforce reductions drove unusually high totals.

Technology accounted for the largest share of May job cut announcements, and artificial intelligence (AI) led stated reasons for cuts for the third consecutive month. Challenger reported 38,579 AI-related cuts in May, equal to 40% of all announced cuts that month. Our read of the data indicates selective restructuring, especially in technology, rather than broad labor market stress.

Investors watch jobs data closely because employment and inflation both shape Federal Reserve policy. Stronger payroll growth gives the Fed less urgency to cut interest rates, especially when inflation remains above the central bank’s long-term target. At the same time, low quits, selective hiring and rising layoff announcements show the labor market still has pockets of caution beneath the solid headline payroll numbers.

“The labor market remains strong enough to support the expansion, and recent payroll gains reduce the Federal Reserve’s incentive to cut rates,” says Bill Merz, head of capital markets research for U.S. Bank Asset Management Group. “Persistent inflation keeps pressure on policymakers, with recent comments from Fed members highlighting the debate shifting toward being prepared to hike rates if inflation remains elevated since the labor market appears to pose less of a risk.” CME Group-derived interest rate probabilities showed markets assigning meaningful odds of a possible increase in the federal funds target rate by year-end as of June 8, 2026, while the Federal Reserve will release its updated projections at its two-day meeting ending June 17. 2

The May jobs report supports a balanced investor view. The economy continues to create jobs, unemployment remains steady and wage gains still support household income. Those trends help limit near-term recession risk and support consumer spending, even as higher prices reduce some of the benefit from rising pay.

“This jobs market update should reassure investors that the economy still has support from employment and income growth,” says Tom Hainlin, national investment strategist with U.S. Bank Asset Management Group. “It should also remind them that steady job gains and persistent inflation can keep interest rates range-bound until the path becomes clearer.” In practical terms, stock and bond markets may continue to react sharply to each new labor or inflation release.

For investors, the May jobs report reinforces the value of staying balanced rather than reacting to one data point. Steady job growth supports the economy, but persistent inflation and changing Fed expectations can still influence interest rates, bond yields and stock market leadership. If you are weighing how labor market trends affect your investment plan, consider working with a financial professional to align portfolio decisions with your goals, time horizon and risk tolerance.

The labor market is a major driver of economic health in an economy where consumer spending comprises more than two-thirds of economic activity. When employment is high, consumer incomes are usually rising, supporting consumer confidence and typically leads to increased spending on goods and services. This accelerated spending often leads employers to add workers to satisfy growing goods and services demand. While the economy can experience periods of slower growth, the long-term trend is an expanding economy, which results in long-term job and income growth.

A strong employment environment often boosts incomes which often drives rising consumer spending. Consumers are considered the driving force of economic growth. According to the U.S. Bureau of Economic Analysis, consumer spending represents more than two-thirds of U.S. economic growth. When individuals are employed and earning solid wages, healthier economic growth often follows. Full-time employment provides households with predictable cash flow, making it easier to make long-term commitments that require financing, such as home and auto purchases.

Structural changes tied to fundamental shifts that affect how work is done often influence labor market trends. For instance, in the past, there was a structural shift from agricultural work to factory work as society became more industrialized. More recently, technology advances sparked an upturn in jobs tied to technology, or jobs that use technology to complete tasks. Today, many economists expect artificial intelligence advances to again create structural labor market changes and expand productivity. This could affect the types of jobs available and labor supply trends.

Labor force participation, a measure of the share of the population working or actively seeking work, has declined from its previous peaks. This decline is due in large part to workforce demographics, specifically the nation’s aging population and immigration changes. According to U.S. Bureau of Labor Statistics data, the labor force participation rate peaked at 67.2% in 2001 and now stands below 62%. Nearly one-quarter of the nation’s workforce is age 55 or older, and the “exit rate” due to retirement outpaces the entry rate of younger generations.

Technological advancements often create anxiety about the labor market impact. Technology and job requirements are constantly changing. Recent artificial intelligence (AI) advancements make this issue even more topical. In previous periods, technological advancements often involved automation replacing certain physical tasks. Today, AI may augment cognitive tasks, possibly changing skill demand in the economy.

Labor market signals can be a guide to current or forthcoming economic conditions. In other situations, labor data may not provide clear guidance. For example, when job growth appears strong, the numbers could be deceptive because hiring may be concentrated in narrow sectors of the economy or in less productive roles. If unemployment remains steady but hiring numbers are sluggish, it could indicate that companies are “hoarding” employees if it becomes challenging to replace them, while adding few new hires.

These data points should not be considered in isolation. Hiring and layoffs should be assessed together. Rising layoffs may raise alarms. Low layoff rates may reflect companies' reluctance to lose staff or indicate a challenging hiring environment. Hiring numbers and job openings reflect labor demand, but they may be lower even in a solid economic environment if companies retain staff and take a more cautious approach to adding overhead. The quit rate is a strong barometer of worker sentiment. A high quit rate reflects worker confidence that other jobs are readily available.

The job market is a key economic indicator, but it should be assessed alongside other indicators. The labor market and inflation are closely connected. If wages rise considerably, it’s important to assess that increase on an after-inflation basis to determine how much workers are benefiting from the wage environment, which translates to spending growth potential. Strong employment numbers typically signal a healthy economy.

The job market connects people looking for work with employers searching for talent. A strong job market signals a healthy, growing economy, as companies add jobs and compete for workers. When unemployment rises and job growth slows or declines, it often points to an economy that’s losing momentum.

The U.S. Bureau of Labor Statistics tracks the unemployment rate every month, giving us a clear view of the nation’s economic health. A lower unemployment rate usually means the economy is strong. This rate draws close attention because it shows how many people are actively seeking work. However, it doesn’t count those who have stopped looking or consider themselves out of the workforce.

When unemployment rises, it signals that the economy may be weakening. People often cut back on spending if they worry about losing their jobs, which can slow the economy even more. On the other hand, low unemployment typically reflects a robust and expanding economy.

The S&P 500’s recent rollercoaster performance has investors wondering what lies ahead for the stock market.

We can partner with you to design an investment strategy that aligns with your goals and is able to weather all types of market cycles.