Capitalize on today's evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

The U.S. economy continues to grow, which lowers near-term recession risk.

Consumer spending and job growth remain positive, though inflation and slower hiring require attention.

Investors should focus on economic and corporate fundamentals, diversification, and long-term goals rather than short-term recession headlines.

The economy exhibited positive momentum in 2026 as the government reopened and business investment improved, all under the shadow of conflict in the Middle East. Corporate profit growth continued surging and companies increased spending on equipment and intellectual property, including technology and software. 1 Consumer spending continued to support broader economic growth, despite a late first quarter rise in energy costs. 2 Markets now face a constructive backdrop, with earnings and economic growth fueled by resilient household and business activity, despite risks including higher costs, a cautious Federal Reserve (Fed) interest rate policy and geopolitical uncertainty.

The U.S. economy continues to expand despite geopolitical tensions, including conflict involving Iran and uncertainty around oil supply. Recent data point to a transition rather than a contraction. Growth no longer matches the faster pace seen in mid-2025, but consumers continue to spend, businesses continue to invest, and key drivers of the economy remain intact. 2

Inflation adds complexity to the growth story. Price pressures have moved higher in some areas, which gives the Fed less room to cut interest rates quickly. 3 This combination creates a more selective environment for investors, where corporate earnings strength fuels longer-term trends but pricing power and policy developments can drive near-term market volatility.

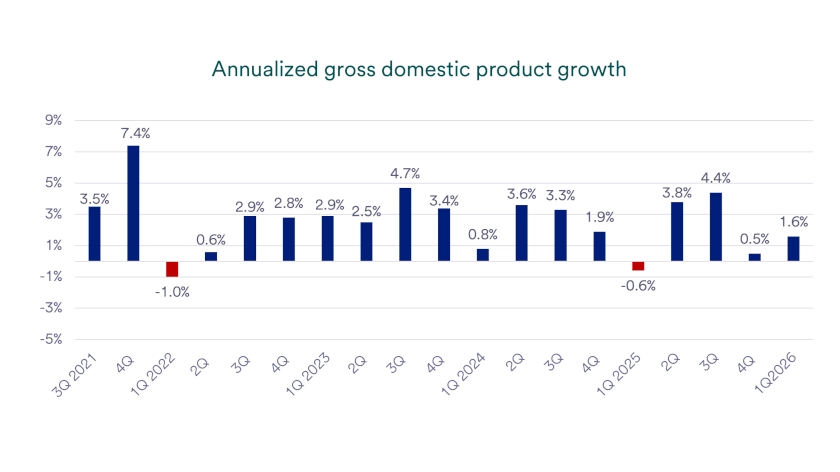

First-quarter gross domestic product, or GDP, showed a clear rebound in economic activity. According to the Bureau of Economic Analysis, real GDP rose at a 1.6% annualized rate in the first quarter, improving from just 0.5% in the fourth quarter of 2025. 2 That improvement suggests the economy regained traction after a slower finish to last year.

Business investment provided the strongest support. Spending increased on equipment, intellectual property products, and private inventories, while residential and nonresidential structures declined. That pattern shows companies continued to invest in productive capacity, including technology and software, even as higher costs and geopolitical risks complicated the outlook.

The broader private sector also remained solid. Real final sales to private domestic purchasers, which combine consumer spending and business fixed investment, increased 2.4% in the first quarter, after rising 1.8% in the fourth quarter. Inflation readings released with the GDP report explain why the Fed remains cautious, as the price index for gross domestic purchases rose 3.5% in the first quarter after a 3.7% gain in the prior quarter. 2

Consumer spending remains a critical driver of the U.S. economy, and household choices continue to shape both growth and corporate profits. A variety of metrics suggest consumer spending remains robust. Official government data from the Bureau of Economic Analysis’ April Personal Consumption Expenditures (PCE) rose 5.9% year-over-year. The Census Bureau’s retail sales figures from the less-volatile control group also rose nearly 5% year-over-year through April. More recently, Fiserv’s preliminary May point-of-sale data indicate over 7% year-over-year growth in spending, supported by Johnson Redbook’s weekly retail sales through late May rising 9% from year-ago levels. That pace fits an environment increasingly driven by higher income consumers, while lower income households remain stretched, forcing more deliberate choices about where to spend.

“Data show that consumer spending remains solid, despite high interest rates and higher costs pressuring lower- and middle-income consumers.”

Bill Merz, head of capital markets research for U.S. Bank Asset Management Group

Fiscal policy also impacts consumers. New tax legislation in 2025 resulted in higher tax refunds this spring for individuals, providing temporary cushion against higher energy prices. So far in 2026, individuals received nearly $50 billion more in refunds than at the same time last year, with refunds on pace to exceed 2025 by $61 billion this year. 4

Bill Merz, head of capital markets research for U.S. Bank Asset Management Group, notes, “Data show that consumer spending remains solid, despite high interest rates and higher costs pressuring lower- and middle-income consumers.” That pressure does not mean consumers stop spending, but it can change what they buy, when they buy it, and which companies benefit. For investors, those spending shifts can separate businesses tied to essential needs from businesses that rely more heavily on discretionary purchases.

The labor market adds another important layer to the consumer story. Steady paychecks often help households maintain spending even when prices rise or credit costs remain elevated. In April 2026, payrolls increased by 115,000 after a solid 178,000 gain in March. 3

Average 2026 job gains so far this year of 76,000 per month compare to 10,000 monthly on average in 2025 and 122,000 monthly in 2024. The unemployment rate held at 4.3%, in line with March and slightly below February’s 4.4% rate, which signals stable labor conditions on the surface. 3

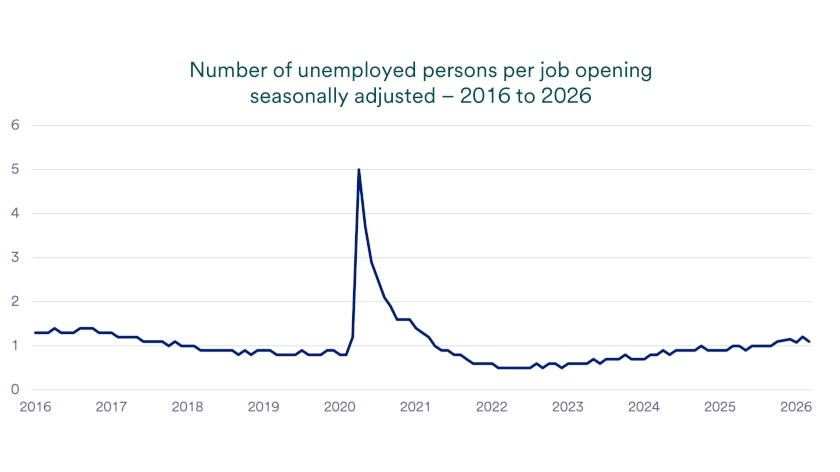

Other labor market measures paint a mixed picture. Initial jobless claims remain low, consistent with recent years posting strong labor market growth. 5 Job openings totaled 6.9 million, indicating a gradual trend lower and below the 7.2 million people counted as unemployed. Wages rose 3.6% from a year earlier. 3 Those numbers suggest hiring demand has cooled, but income growth still gives many households a foundation for continued spending.

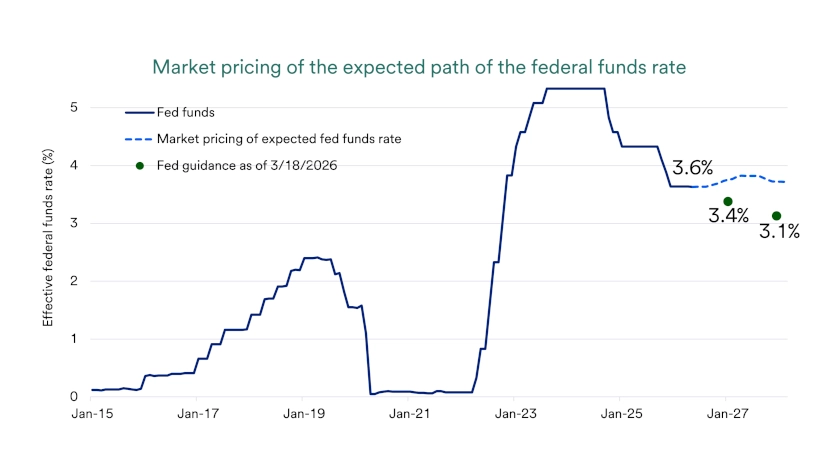

The Fed has held interest rates steady so far in 2026 after cutting rates by 1.75% over the course of 2024 and 2025. Outgoing chair Jerome Powell has emphasized that the path ahead remains uncertain, and recent data support a patient approach, particularly with the recent energy price shock beginning to spill over to other prices. Complicating the picture further, new Fed Chair, Kevin Warsh, has expressed a preference for lower policy rates despite many on the voting committee favoring a wait-and-see approach.

Market pricing also points to a slower path for additional easing. 6 Market expectations now lean toward no cuts, and outdated projections from the March Fed meeting indicated a median expectation for one cut this year. 7 Policy rate timing affects investors because borrowing costs influence mortgages, auto loans, credit cards and the financing decisions companies make when they expand.

The investment backdrop includes support and friction at the same time. Ongoing economic growth, steady consumer demand, and robust business spending continue supporting corporate earnings, and recently drove stocks to new all-time highs. Fiscal policy support in the form of higher tax rebates buy time for a resolution to energy supply constraints. At the same time, uncertain interest rate policy, higher costs, and shifting policy headlines can move investor sentiment quickly.

Investors should consider a number of economic indicators when assessing current economic conditions. These include data on Gross Domestic Product (GDP) growth, inflation, the unemployment rate and other labor market indicators, consumer and business spending, and interest rates. A healthy economic scenario often includes rising GDP, low unemployment, and stable inflation near the 2% level. A recession is typically defined by two consecutive quarters of GDP contraction, often accompanied by a weak labor market, such as rising unemployment.

The economic cycle (or business cycle) tends to move through stages. The expansion phase features rising Gross Domestic Product (GDP), low unemployment, and rising consumer activity. Rising inflation (reflected in increased cost-of-living) may also result. During the economic cycle, activity eventually peaks and a slowdown begins with slower GDP growth. In some cases, that slowdown leads to a recession, where GDP contracts for a period of time. The lowest point of the economic cycle, a trough, is followed by an economic recovery, where GDP again moves into positive territory.

Several factors can influence economic growth through a cycle. These include Federal Reserve monetary policy, particularly the decision to raise or lower interest rates; policies that favor narrow groups of industries rather than the broad economy; and external pressures such as elevated inflation or geopolitical conflicts. These variables can alter the economic environment, often in unpredictable ways.

Investors do not need a perfect forecast to make thoughtful decisions. A clear plan, which spans multiple business cycles, tied to your goals, time horizon, and risk appetite can guide choices when recession headlines, inflation reports or interest rate expectations shift. A conversation with a wealth management professional can help translate economic signals into practical steps that fit your situation.

Note: Diversification and asset allocation do not guarantee returns or protect against losses. The Standard & Poor’s 500 Index (S&P 500) consists of 500 widely traded stocks that are considered to represent the performance of the U.S. stock market in general. The S&P 500 is an unmanaged index of stocks. It is not possible to invest directly in the index. Past performance is no guarantee of future results.

What is a recession? A recession is a broad and sustained decline in economic activity. People sometimes use two straight quarters of falling GDP as a quick rule of thumb, but that shortcut can miss important details. In the U.S., the National Bureau of Economic Research weighs several measures, including jobs, production, income, sales, and GDP, and it often makes its determination after a downturn has already begun.

When was the last recession? The most recent recession began with the COVID-19 shock in early 2020. It lasted only a few months, but it was severe because shutdowns quickly disrupted work and spending. The prior recession was the 2007–2009 period tied to the financial crisis.

No one can predict recessions with certainty, and the economy can change quickly. Today’s data still show growth and ongoing consumer spending, which generally lowers near-term recession risk. The key things to watch include job trends, credit conditions, and whether inflation stays high enough to keep interest rates restrictive for longer.

The S&P 500’s recent rollercoaster performance has investors wondering what lies ahead for the stock market.

We can partner with you to design an investment strategy that aligns with your goals and is able to weather all types of market cycles.