Capitalize on today’s evolving market dynamics.

With changes to taxes and interest rates, it's a good time to meet with a wealth advisor.

U.S. Treasuries help investors pursue income, liquidity and diversification as interest rates shape prices and returns.

Current Treasury yields appear to compensate investors for Fed policy, inflation, growth expectations and Treasury supply.

Deficit spending deserves attention, but global demand and recent auctions still point to a functioning Treasury market.

U.S. Treasury yields respond to a steady tug-of-war among Federal Reserve (Fed) policy, inflation, growth expectations, and bond supply. These forces influence Treasury prices, shape returns for current bondholders and create new income opportunities for investors putting money to work today. Current yields appear to compensate investors for those core drivers, although U.S. deficit spending could increase future Treasury issuance and deserves continued monitoring.

“Treasuries offer reliable, high-quality income, while adding a unique source of diversification to portfolios.”

Bill Merz, head of capital markets research for U.S. Bank Asset Management Group

For investors building resilient portfolios, Treasuries can serve several roles at once. They can help support stability, provide liquidity and generate income without taking on corporate credit exposure. “Treasuries offer reliable, high-quality income, while adding a unique source of diversification to portfolios,” says Bill Merz, head of capital markets research with U.S. Bank Asset Management Group.

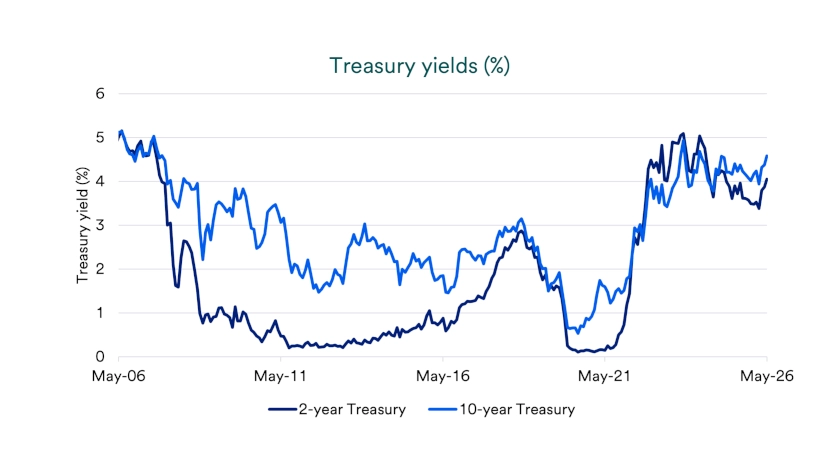

Treasury yields currently range from roughly 3.6 %-5.2%, depending on maturity, giving investors meaningful income opportunities relative to the last 20 years. Even with explicit U.S government backing, Treasury prices often fluctuate before maturity as interest rates, inflation expectations and supply conditions change. Those price moves can influence investors who rebalance portfolios, harvest gains or manage interest rate risk, especially because longer-term maturity bonds tend to react more sharply when yields change.

“Our proprietary fair value model indicates current Treasury prices fairly compensate investors for the risks we evaluate,” Merz notes. In that model, Fed policy rate expectations account for about three-quarters of the fair value yield, making them the dominant long-term driver in this framework. Other forces can still influence yields at the margin, including new issuance tied to deficit spending and the role Treasuries play when investors seek diversification from equities. 1 This framework helps identify which force has the greatest influence on yields at a given point in time. It also helps investors separate near-term market noise from longer-term trends in policy, inflation, and growth.

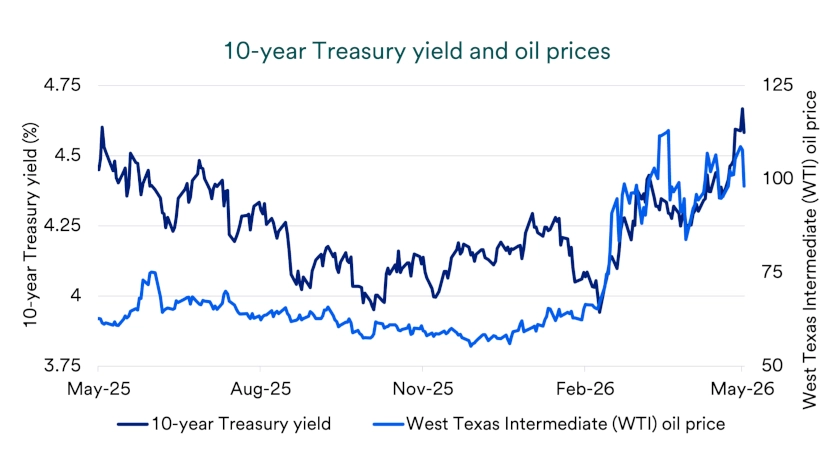

Inflation and inflation expectations remain closely linked to Treasury yields because inflation erodes the purchasing power of fixed coupon payments over time. Today, Treasury yields are high enough to provide an income stream above expected inflation. A 10-year Treasury yield of approximately 4.5%, compared with 2.5% expected inflation, implies a buy-and-hold investor could expect a “real” or inflation-adjusted return of about 2.0%.

Inflation can also influence bond prices before maturity. Oil prices have risen in 2026, lifting inflation expectations and changing how investors assess the likely Fed policy response. Market prices have shifted from an expected Fed interest rate cut to the possibility of an interest rate hike in 2026 to quell potential inflation. Treasury yields rose and bond prices fell as investors demanded more income return to compensate for inflation risk and rate hike expectations, although long-run growth and inflation trends still suggest Treasuries reasonably reflect underlying economic conditions.

The Fed can shape Treasury yields through two primary channels: the policy rate and the size of its balance sheet. By setting the federal funds rate, an overnight lending rate between banks, the Fed establishes a baseline that most directly affects bank borrowing costs and short-term Treasury yields. Longer-term yields then respond as investors weigh whether to reinvest in shorter maturities or lock in longer-maturity income.

The Fed reduced its target short-term rate by 1.75% across 2024 and 2025, bringing the target range to 3.50-3.75%. Current interest rate pricing implies investors expect that the Fed may remain cautious as it balances inflation, energy prices and labor-market conditions.

The Fed can also influence Treasury yields by buying or selling Treasuries for its own account. The Fed recently shifted from reducing its Treasury holdings, by not replacing maturing bonds, to gradually buying short-term Treasury bills, primarily to support smooth funding-markets functioning. That purchase activity means private investors absorb less aggregate supply, which can help steady yields at the margin.

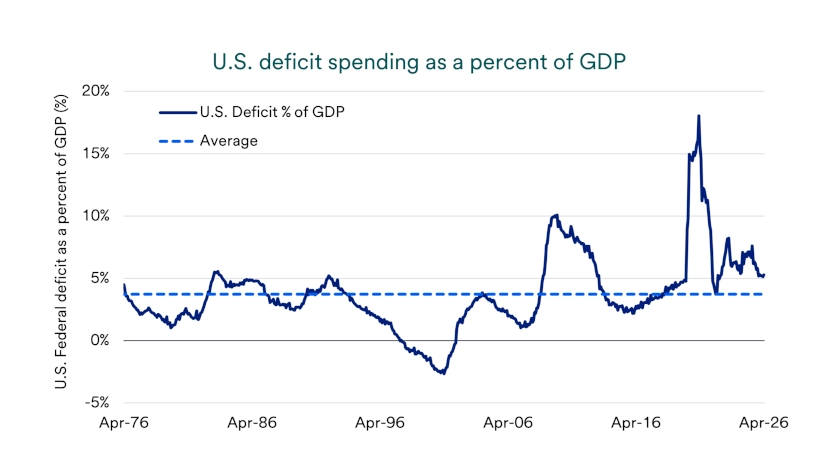

America’s fiscal trajectory remains a focus for investors, especially with the federal deficit exceeding 5% of gross domestic product. Ratings agencies have cited that backdrop in recent warnings, including Moody’s downgrade of U.S. debt in 2025, Fitch’s downgrade in 2023 and S&Ps downgrade in 2011. Financial markets reacted only mildly, however, with U.S. bonds performing largely in line with bonds from other developed economies during the same period.

“We do not see strong evidence of the U.S. fiscal situation heavily influencing bond yields right now based on our calculations, but we must monitor government, economic and market data for signs of change,” says Merz. Federal government policy choices, including deficit spending, tax and tariff changes can still alter the deficit path. The Congressional Budget Office projects elevated deficits over the next decade as spending exceeds tariff and tax revenue.

The U.S. Treasury Department has recently relied on higher short-term bill issuance to fund government spending that exceeds receipts. That approach has helped prevent increased supply from lifting intermediate- and long-term yields. The Treasury stated in May 2026 that it plans to continue this policy, keeping medium- and long-term bond auction sizes stable for the next several quarters, although continued deficit spending could eventually require greater issuance in those maturities.

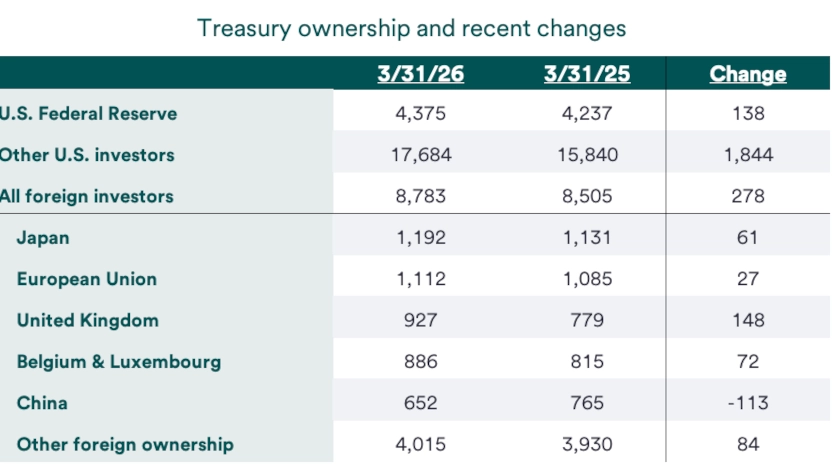

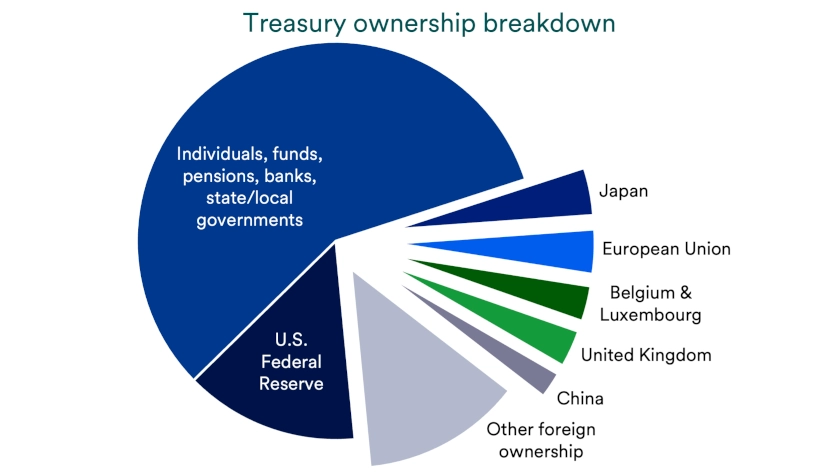

Recurring headlines suggest foreign investors may step away from U.S. assets, but recent data tells a different story. International buyers increased their Treasury holdings by nearly $300 billion over the 12 months through March 2026. That demand provides important support for Treasury prices, even when investor sentiment shifts.

Concerns about a foreign investor buying “strike”, which could lift yields, have not shown up in market prices. “We see no evidence of a buyers’ strike based on the data,” says Merz. Investors should still consider that scenario as a risk, but current market evidence does not suggest a broad retreat from Treasury demand.

Treasury auction results provide another real-time window into investor appetite. Recent outcomes are only slightly weaker than long-run averages and common auction indicators still point to generally normal bond market functioning. “Domestic demand fluctuated over the past couple years on investor inflation and deficit concerns, but Treasury auction results are near-normal,” says Merz, and recent regulatory changes could also increase financial institutions’ capacity to hold Treasuries.

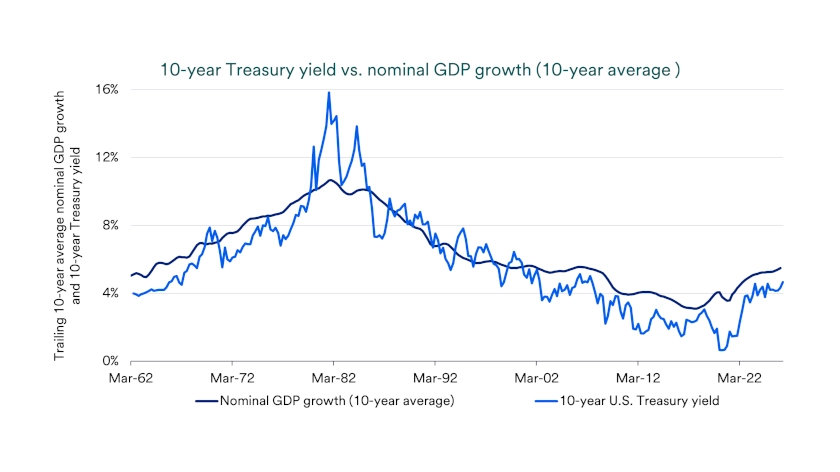

Over long periods, long-term Treasury yields tend to coalesce near nominal economic growth, which combines real growth and inflation. The relationship is not perfect, because unusually loose or tight central bank policy can push yields away from that long-term reference point. Still, nominal growth gives investors a useful way to judge whether long-term Treasury yields look unusually high or low relative to the broader economy.

By this measure, long-term Treasury yields remain within a normal historical range. That does not remove the possibility of short-term volatility, especially when inflation, energy prices and Fed expectations move quickly. It does suggest current yields broadly reflect the economy’s underlying growth and inflation backdrop rather than a clear signal of Treasury market stress.

Treasuries can help investors pursue steadier income while dampening volatility from riskier asset prices. Investors seeking more consistent returns may benefit from larger high-quality bond allocations, while more risk-tolerant investors can use Treasuries as a stabilizing counterweight. Because high-quality bonds often move differently than stocks and other higher-risk assets, Treasuries can support diversification aimed at managing overall portfolio volatility.

U.S. Treasuries remain a core holding for many diversified portfolios. The market has adapted to higher issuance so far through broader participation and regulatory support. Today’s yields offer meaningful income opportunities that fairly compensate investors for policy expectations, supply, inflation, and diversification properties.

Treasury securities are debt instruments issued by the U.S. government to fund spending in excess of current tax receipts and replace maturing securities. When investors buy Treasuries, they lend money to the federal government. Depending on the type of Treasury security, the government makes regular interest payments to investors. When the security matures, investors receive the full face value of their investment.

As funding needs arise, the U.S. government offers new Treasury securities through a public auction system. Large financial institutions submit competitive bids by stating the yields they are willing to accept. The auction process helps set the yield for each security, including the yield individual investors receive when they participate through non-competitive bids.

Investors find the Treasury market attractive for several reasons. Most importantly, Treasuries are backed by the full faith and credit of the U.S. government, which means investors generally view them as among the safest available investments. Investors can typically rely on timely interest payments and full repayment of the full face value when the security matures.

Treasuries also trade in a large, active global market, which makes them easier to sell for cash than many other investments. Interest payments are completely exempt from state and local income taxes, although federal taxes still apply. In addition to providing high-quality income, Treasuries can help diversify investment portfolios because their prices often move differently than stocks and other higher-risk investments.

The U.S. Treasury market plays a central role in the broader financial system. Investors generally view Treasuries as among the safest assets because they carry the backing of the U.S. government’s full faith and credit. As a result, many investors use Treasury yields as a comparison point for other types of fixed-income investments.

Rates on other debt securities generally exceed Treasury rates because those investments carry more risk. Many global institutions also use Treasuries as collateral for large financial transactions because buyers and lenders widely trust their value. The Federal Reserve (Fed) may buy or sell Treasuries to help maintain its target interest rate and influence economic conditions. The reliability of Treasuries also supports the U.S. dollar’s role as the world’s primary reserve currency, while global demand for dollars helps support demand for Treasuries.

A variety of factors influence Treasury supply and demand. When demand is high, Treasury prices tend to rise and interest rates tend to moderate because prices and rates move in opposite directions. When demand declines, the federal government usually must offer higher yields to attract investors.

Investor demand often reflects the need for safety, income and flexibility. Some institutions also buy Treasuries because rules or investment guidelines require them to hold high-quality assets. Investors may find Treasuries attractive compared with similar investments, such as corporate bonds or foreign government bonds.

Federal deficit spending is the primary driver of Treasury supply. When government spending exceeds tax revenue, the U.S. Department of Treasury issues more securities to fund the difference. Congress also must periodically address the federal debt ceiling so the Treasury can continue issuing securities needed to meet the government’s obligations.

Treasury market trends can offer useful signals about the economy and investor expectations. Most of the time, short-term Treasury securities offer lower yields than longer-term Treasuries. Investors usually accept lower yields for lending money over shorter periods and expect higher yields for committing money for longer periods.

This normal pattern, often called a normal yield curve, typically points to expectations for a healthy, growing economy. An inverted yield curve occurs when shorter-term Treasury yields rise above longer-term Treasury yields. This often reflects higher current or expected Fed policy rates and concerns about slower growth. An inverted yield curve can serve as a recession warning signal, although it does not always lead to a recession.

Investors should still monitor the risks that can shift Treasury yields and bond prices. Fed policy, new legislation, issuance patterns and inflation expectations can all change the income outlook. Discuss your portfolio positioning with a U.S. Bank wealth professional to determine how U.S. Treasuries may fit alongside your income needs, risk tolerance and long-term investment objectives.

Treasury bonds can offer higher income when yields are elevated, but prices can still fluctuate before maturity. Investors should match maturities and allocation size to income needs, risk tolerance and time horizon.

Treasury yields respond to Federal Reserve policy, inflation expectations, economic growth, Treasury supply and investor demand. Short-term yields tend to track Fed policy more closely, while longer-term yields also reflect inflation, growth and fiscal expectations.

Treasuries can provide high-quality income and may help offset volatility from riskier assets. Their role depends on the investor’s goals, liquidity needs and broader asset allocation.

Municipal bonds currently offer tax-sensitive investors compelling return opportunities.

We can partner with you to design an investment strategy that aligns with your goals and is able to weather all types of market cycles.